For decades, football has turned its jersey into a prime advertising medium. What has shifted is the scale. According to the latest data from the European Sponsorship Association (ESA), football generated more than €13 billion in sponsorship value in 2025, within a European market that approached €34.5 billion. The five major leagues accounted for €12.5 billion of that total. The shirt—both the one worn by players and the replica sold by the kit manufacturer—remains the most coveted asset.

For the first time in history, all 96 clubs in the Premier League, LaLiga, Serie A, Bundesliga, and Ligue 1 have at least one main shirt sponsor. This milestone was completed by Lazio, which signed a deal with Polymarket, a prediction market platform, in April 2026. This fact speaks volumes about the market’s evolution: a decade ago, no one would have predicted a club displaying a company from that sector on its chest.

**The Dominance of Three Brands**

In the kit business, the landscape has been set for years. Adidas, Nike, and Puma control more than half of the 96 clubs and dominate the ten most lucrative contracts in the market. The remainder is contested by between 10 and 15 smaller brands, primarily Macron and Joma, which split the mid‑table and lower‑table clubs, competing on price, design, and commercial flexibility.

The scale of the largest contracts is hard to grasp. The ten biggest deals exceed €50 million per year in base value, not including variables. Barcelona, Real Madrid, Manchester City, and Manchester United are all above €100 million. Adidas holds five of those ten contracts, Nike four, and Puma one—Manchester City’s. All agreements run until at least 2030, with some, like Juventus’s with Adidas, extending to 2037.

However, the absolute value of a contract does not tell the whole story. The level of dependence it creates matters. For Chelsea, Arsenal, Juventus, and Manchester City, the kit supplier deal accounts for about 30% of their commercial revenue. Bayern Munich, Liverpool, and Paris Saint‑Germain are well below that threshold—between 14% and 19%—reflecting much more diversified commercial structures.

**The Airline as Universal Sponsor**

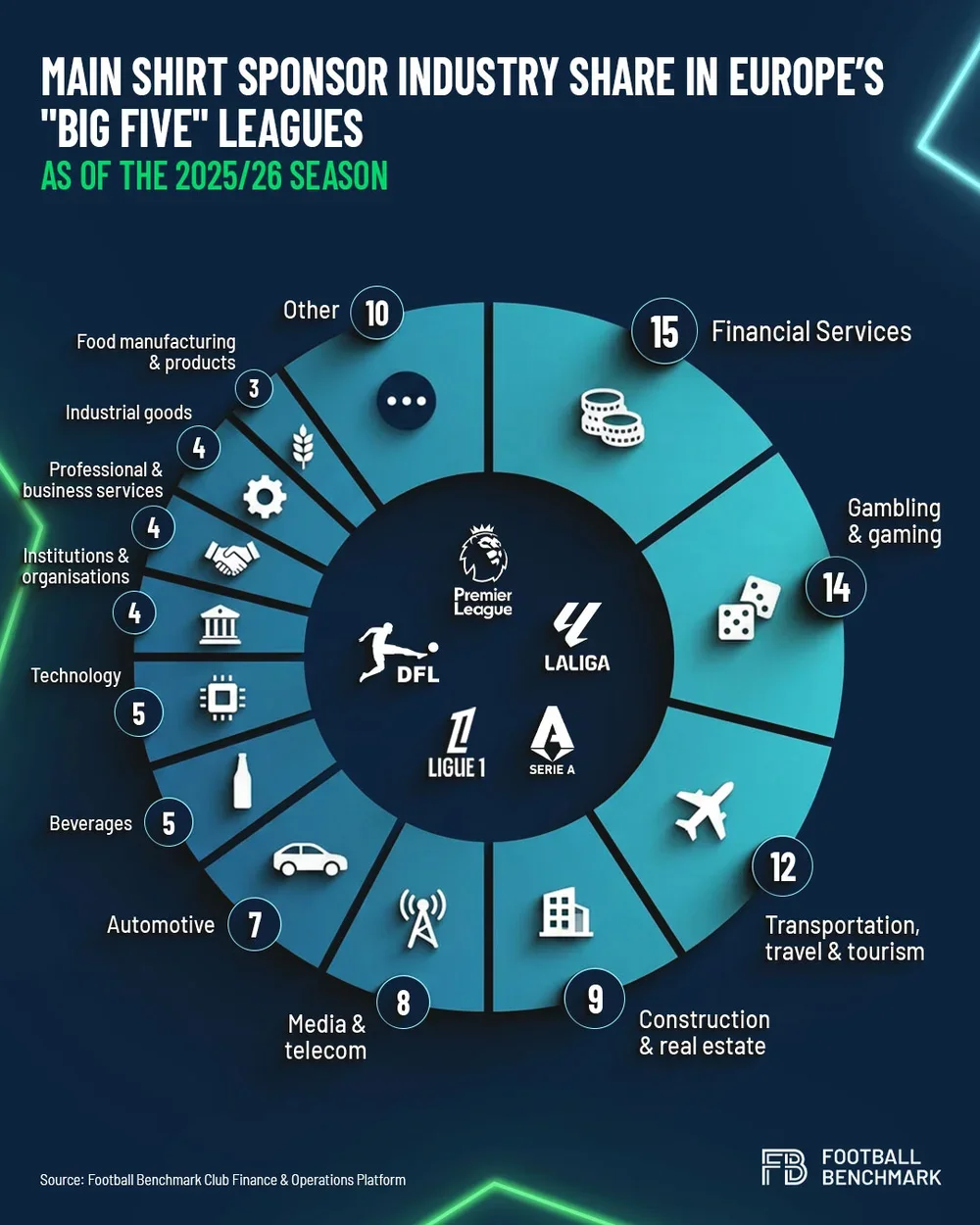

On the shirt sponsor front, the market is far more diverse. Close to 20 different sectors have a presence among the 96 clubs. The most represented are financial services, betting and gaming, and transport and tourism. Together, these three sectors account for 42% of the market.

Within the transport category, Gulf airlines have turned European football into their primary global showcase. Emirates, Qatar Airways, Etihad, and Riyadh Air jointly sponsor eight clubs. And in the ranking of the ten most lucrative shirt contracts, five are with airlines. No medium moves global audiences like the football of the five major leagues, and no industry needs global visibility more than long‑haul aviation.

The market is also markedly international. Out of the 108 active main sponsorship agreements across the five leagues, nearly half involve foreign companies. In the Premier League, that figure reaches 100%: no shirt sponsor is based in the UK.